How much does it cost to sell a property at auction? A guide for UK property owners. How much does it cost to sell a property at auction and how do the sale costs compare to an estate agency sale? Find out about the costs for selling your house or flat at auction and how to save money by passing some of your costs to the buyer.

How much are property auction fees?

Selling a property at auction costs less than most people think. The total cost is about the same you would expect to pay a traditional high street estate agent. There are 3 costs to consider when selling a property at auction:

- (1) COMMISSION - The auctioneers commission is around 2% to 3% + VAT of the final sale price and that's only paid when the property successfully sells.

- (2) ENTRY FEE - Most auctioneers request an upfront catalogue/entry fee of around £300 + VAT or more, but it may be possible to postpone payment until after the property has successfully sold.

- (3) AUCTION LEGAL PACK - The seller's solicitor is responsible for preparing the auction legal pack at the cost of £200 or more, which is payable before the auction.

Passing your auction sale costs to the buyer

A key benefit of selling at auction is the complete control the seller has over the contract of sale, there's no input from the buyer. This means the seller can dictate terms like the completion date, responsibilities of the buyer after exchange and any extra costs to be paid by the buyer.

By adding a simple clause to the contract of sale it's possible to pass all (or part) of your auction costs and legal fees to the buyer, in fact it's standard practice for regular auction sellers (e.g. property traders, banks and local authorities). Some buyers will not bid as high for the property if they spot the clause in the legal pack, but others will not worry.

Negotiating sales commission with the auctioneer

The starting rate for an auctioneer's commission is typically 2% to 3% + VAT and that's only paid when the property successfully sells. So if a property sells for £200,000 the commission payable to the auctioneer at 2% would be £4,000 + VAT.

You can save money by passing costs to the buyer. And some auctioneers offer a no sale no fee service.

For higher value or particularly saleable properties the auctioneer might be prepared to reduce their commission, but there is a lot of organising and marketing that takes place for the auctioneer to be able to justify their fee.

Auctioneers usually charge a minimum selling fee of anything from £1,500 upwards, so if a low value property (such as a garage) sells for £10,000 the 2% commission rate will not apply, otherwise the fee would only be £200. Instead the auctioneer will charge the minimum selling fee.

TIP: Compared to some of the newer methods of selling, such as paying an online estate agent a fixed fee, selling a property at auction may seem relatively expensive. So it's worth a quick cost benefit analysis to see if auction will pay off for you.

How much does it cost to prepare the auction legal pack?

The auction legal pack is crucial for the successful sale of a property at auction, it contains all the legal information (e.g. land registry documents, deeds, searches, property information questionnaires, lease documents, tenancy agreements etc) relating to the property. So the more information there is in the legal pack the more confident prospective buyers will be when bidding on auction day. It's therefore important not to cut costs when preparing the legal pack as it may adversely affect the final sale price. Costs for preparing an auction legal pack for a freehold property can be anything from £200 upwards. For a leasehold property the cost of obtaining the management information pack from the freeholder/landlord will add another £200 or more.

Most of these legal costs are not unique to selling at auction. When selling through an estate agent or privately the seller will also need to prepare legal documents for the prospective buyer. It's only the searches (local authority search, water search etc) that are obtained by the buyer in the case of an estate agency sale, but by the seller in the case of an auction sale.

Who pays for the survey?

We're occasionally asked whether the seller needs to include a survey report for their property in the auction legal pack. The survey report is NOT the responsibility of seller. There is no expectation for a survey report to be included in the auction legal pack.

Many of the buyers at auction are cash buyers, so will not require a survey. However, if the buyer does require a survey, they will need to have sorted that out (and seen the report) before bid on auction day. With an unconditional auction sale, the buyer is bidding to buy - full stop! They're not bidding to buy subject to contract or survey.

Costs for selling a house by auction?

Request a free valuation and auction sale cost estimate for your property today. In some cases we may need a few more details about your property before providing a free and no-obligation auction sale estimate.

Free EstimateCosts for cancelling or withdrawing from auction

If you've booked your property into auction, but then have a change of plan, you may be liable to paying the auctioneers withdrawal fee if you decide to back out of the auction sale. Auction withdrawal fees vary, but can be as much as the full commission rate you would have been liable to pay if your property had successfully sold.

It's worth noting that if you signed the auctioneers' terms remotely (i.e. not in the auctioneers office) there will usually be a 14 day cooling off period. However, since the timescales for selling at auction are very quick, the auctioneer might ask you to tick a box on the auction contract that waives your right to cancel, in order for them to commence their service immediately, and begin marketing your property as soon as possible.

Other costs to consider when selling a property at auction

As with selling a property through an estate agent or privately, there are other costs to be considered when selling a property, they include; legal fees, moving costs and taxes that might be due. For example capital gains tax on buy-to-let properties and inheritance taxes for probate sale. Also consider whether any early redemption penalties might be due on your mortgage or secured loans. These are all payments your solicitor will be able to help you calculate when determining your bottom line sale price i.e. your reserve price.

If the property doesn't sell at auction there will usually not be any costs or obligations to the seller, unless stated in the auctioneers terms.

Are there any costs to pay if a property fails to sell at auction?

Just like selling through a traditional high street estate agent, the auctioneers commission works on a "no sale no fee basis". So the sales commission is only payable when the property is sold and contacts are exchanged, without that happening the auctioneer won't charge their fee. If a property fails to sell the only costs incurred by the seller would be their legal fees (for preparation of the auction legal pack) and any entry/catalogue fee that may have been paid before the auction.

Cost benefit analysis - is it worth selling at auction?

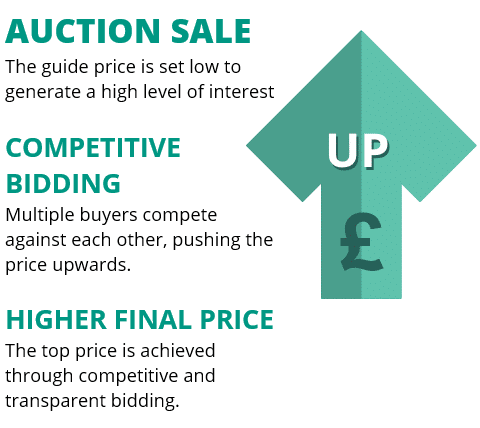

With so many low-cost online estate agents to choose from, does an auction sale provide value for money? Apart from the speed and reliability an auction sale offers, from a purely financial perspective, is it worth it? Can you achieve a higher sale price at auction compared to any other method of sale? The answer depends on the type of property being sold, some properties sell for considerably more at auction compared to estate agency sales due to two key features of auction; competition and transparency.

Competition

Property developers, amateur DIYer's and ambitious owner occupiers will compete to buy a property at auction in the knowledge they'll be able to refurbish it cost-effectively and either sell on for a profit or live there themselves. The key word being compete. In an auction environment, where the price can only go one way (up) it's the competitive bidding environment that drives the price up.

Transparency

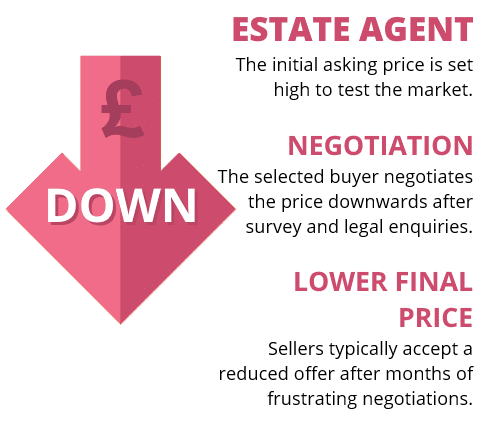

In a closed/private sale environment, such as an estate agent sale (also known as a "private treaty" sale) the estate agent has a high level of influence over negotiations. If after a few months of marketing a property the estate agent tells the seller that £100,000 is a fair price, the seller will probably be inclined to accept an offer around that level. By keeping the property in the hands of one or two estate agents the sale lacks transparency.

In fact, a highly lucrative market exists for property traders who purchase problem properties through estate agents one week and flip them at auction the next week - the properties are sold for considerably higher prices as "properties with potential" in the transparent and competitive bidding environment that's found at public auction.

Ready for auction?

Request a free valuation and reserve price estimate for your property today. In some cases we may need a few more details about your property before providing a free and no-obligation auction sale estimate.

Free EstimateQuestions and Answers

Do properties sell for lower prices at auction?

Some types of property are particularly well suited to sale by auction; properties in need of modernisation or with potential are ideal for auction and will achieve a higher sale price at auction compared to an estate agency sale. But properties with their potential exhausted will usually sell for more by private treaty (estate agency) sale, unless the property is unique or in a very good location, in which case the top price may be found through competitive bidding at auction.

What happens if an auction property doesn't sell?

Most properties do successfully sell at auction, it's considered the most reliable method of sale. If bidding doesn't reach the reserve price on auction day your property will be made available as an unsold lot. The auction company will contact all interested buyers and ask for their best and final offers. If a property doesn't sell first time around it can be entered into a subsequent auction, that might be 4 or 6 weeks later.

What costs are paid upfront and after an auction sale?

The costs for selling at auction works out to be about the same as using a good high street estate agent. Commission at around 2% to 3% + VAT if the final sale price is only payable on successful sale. Some auctioneers charge an upfront entry fee of £200 to £500, but this can be negotiable and only payable after sale.

How quickly can a property be sold at auction?

Legal exchange of contracts can take place within 3 to 4 weeks, with completion of sale a further 4 weeks later. Timings are flexible; if a seller needs to complete sooner or later, they can ask their solicitor to shorten or extend the completion date.

How do you find a good local property auctioneer?

There are hundreds of property auctioneers in the UK. The best suited auctioneer for your property will depend on the property type and location. Looking at the past auction results (usually available on the auctioneer's website) can be a good starting point to short list a suitable auctioneer.

Popular auction resources

- Guide to selling your house at auction

- Risks and disadvantages of auction sales

- Frequently asked questions

- Online property auction sale costs

- Request an auction sale price estimate

Next steps...

Why not request a free pre-auction appraisal for your property? It only takes a few seconds. Or feel free to call us on 0800 862 0206 if you have any questions.

UK Property Market Update: August 2026

The housing market has gone into the summer slower than usual. Prices are still edging up year on year, but only just, and the real story is activity: buyers have more choice than at almost any point in the past decade and are taking their time, while sellers are having to work considerably harder to attract them. July was the quietest month of 2026 so far.

The Bank of England held the base rate at 3.75% on 30 July, but the vote was the closest it has been in this cycle and three of the nine members wanted to put rates up. That is the backdrop to plan around this autumn: borrowing costs that are no longer falling, and a market in which accurate pricing is doing all of the work.

House prices and activity

Annual price growth has slowed again. Nationwide put the average home at £277,542 in July, up just 0.1% on the month and 1.8% over the year. Zoopla has annual growth down to 1.3% (from 1.7% a year ago) on an average of £271,900, and expects it to ease further towards 1% by the end of the year. The Lloyds index, formerly Halifax, is softer still at 0.6% annual growth in June on an average of £299,330.

Activity is where the pressure really shows. Zoopla reports sales agreed down 9% on this time last year, with July the weakest month of 2026, and 30% of the homes listed since the spring still unsold without a price reduction. Rightmove's July figures tell the same story from the seller's side: the average asking price for a newly listed home fell 1.0% to £372,359, a much larger drop than the 0.2% that is normal for July, with the supply of homes for sale close to a 12-year high. The regional split persists, too. The North East is the only region where sales agreed are ahead of last year, up around 4%, while the average London home has shed £3,270 over the past 12 months.

One figure is worth holding on to, though: Rightmove found that 74% of the homes that sold did so without any price reduction at all. Buyers have not gone away. They are simply declining to pay for over-optimistic asking prices.

Interest rates

The Monetary Policy Committee held the base rate at 3.75% on 30 July, voting 6 to 3. The three dissenters, Megan Greene, Catherine Mann and Huw Pill, each wanted a quarter-point rise to 4%. Energy prices have remained volatile and above their pre-conflict levels since the disruption in the Middle East, and the members voting for an increase are concerned that this feeds through into more persistent inflation. Where the market began the year expecting cuts, the live debate now is whether the next move is up. The next decision comes on 17 September.

Inflation

There was better news on inflation. CPI fell to 2.6% in the year to June, down from 2.8% in May and the lowest reading since March 2025. The improvement came mainly from transport, where inflation eased to 5.7% from 6.8%, with motor fuels (diesel in particular) doing most of the work. Core inflation, which strips out energy, food, alcohol and tobacco, was unchanged at 2.6%. That is close enough to the Bank's 2% target to take some heat out of the argument, but not so decisively that a cut looks likely before the autumn.

Mortgages

Mortgage pricing drifted the wrong way over the summer. Rates fell to around 4.65% in June before edging back up to roughly 4.75% in July as global uncertainty pushed up funding costs. Across the whole market the average two-year fix now sits at about 5.51% and the five-year at 5.53%, though borrowers with a large deposit do considerably better, at around 4.6% at 60% loan to value. Anyone coming off a fixed rate this year should still budget for higher payments than last time, and is well advised to speak to a broker early.

What does this mean for property auctions?

Auctions are having a markedly better year than the wider market. Essential Information Group recorded 7,738 lots sold in the first quarter of 2026, up 19.5% on the same period in 2025, raising £1.49 billion. That follows a full year in 2025 in which 29,026 lots sold and £5.87 billion was raised, both ahead of 2024. So while private-treaty sales agreed are down 9%, the auction room is busier than it was.

The reason is straightforward. When ordinary sales slow and chains turn fragile, certainty becomes the thing worth paying for. At auction, contracts exchange on the fall of the hammer and completion follows within weeks, with no renegotiation and no chain to collapse. A private-treaty sale, by contrast, now typically takes around five months from accepted offer to completion and carries a real risk of falling through along the way.

The auction calendar itself is just restarting. Most of the established “on-the-day” auction houses take August off, with only a handful of sales this month, and the ballroom auctions resume properly in September. If you want to be in an autumn catalogue, now is the moment to make contact: entries for the mid-September sales are closing over the next fortnight, and the October catalogues shortly after.

What sells well has not changed. Competition remains fierce for refurbishment stock in good locations, the unmodernised or run-down house on a street where everything else has been done up. Builders, developers and cash investors are still bidding those lots well past guide. Flats are a growing part of the picture as well, accounting for roughly a quarter of all residential lots sold in 2025 and up almost 80% since 2021, as leasehold problems and portfolio restructuring push more of them towards auction.

Tenanted property continues to feed the auction room too. With Section 21 “no-fault” evictions abolished from 1 May under the Renters' Rights Act, many landlords would rather sell with tenants in place than go through the courts, and auction is the natural home for that kind of lot, where portfolio buyers bid competitively for a property that arrives with an income already attached.

The message for sellers is unchanged, just sharper than it was a year ago. With buyers spoilt for choice, a realistic guide price is what separates a lot that sells on the day from one that does not. Price to today's market and the results are still excellent.